What 300 Agency Owners Told Us About Their Financial Confidence — Without Saying a Word

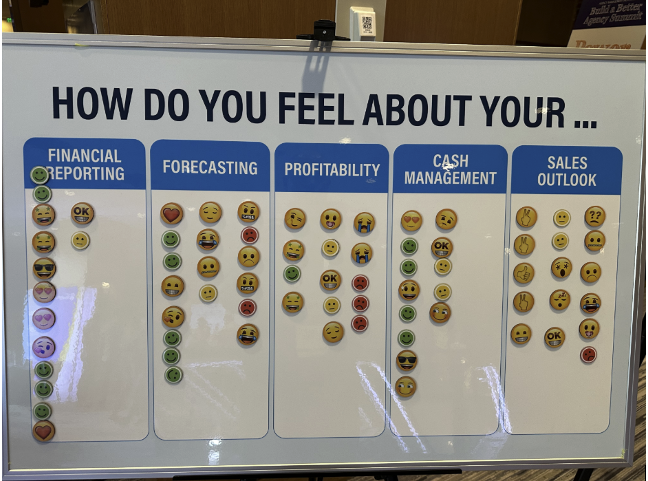

By Tom Wadelton, Virtual CFO and Partner, Anders At this year's Build a Better Agency Summit, hosted by the Agency Management Institute in Denver, our Virtual CFO team ran a simple exercise at the Anders booth. We put up a board with five categories that are the foundations of marketing agency financial management — Financial [...]

{kind=link}

{kind=link}

{kind=link}